Long-Term Care Insurance Quote Service ™

Get a fast and accurate quote from the best companies.

A Guide To Long Term Care Planning

What is your plan if your health suddenly changed?

Many people have asked how best to plan for long term care, so we have put together these web pages where you can find:

- How much it will cost to self-insure.

- Receive quotes from top companies for the benefits you want.

- Apply for LTC insurance (can take 1-2 months for approval).

Because, at least 70 percent of people over age 65 will require some long-term care services at some point in their lives. And, contrary to what many people believe, Medicare and private health insurance programs do not pay for the majority of long-term care services that most people need - help with personal care such as dressing or using the bathroom independently. Planning is essential for you to be able to get the care you might need.

- U.S. Department of Health and Human Services

Long term care may be the biggest risk to your life savings, independence, and quality of life. If you don't think you're at risk today you are in denial.

Your health insurance, Medicare, and Medicaid do not cover what is considered long term care without serious financial consequences to your family and your future.

The fact is that if you had a stroke, car accident, or any number of other changes in health tomorrow you would be totally unprepared for long term care.

The Internet is a great tool that you can use to learn about long term care or you could visit a local nursing home or assisted living facility.

Imagine if you didn't have homeowners insurance, car insurance, or health insurance, how would you feel? That's how people feel once their health changed.

Every year, in addition to thousands of auto and other accidents, there are 700,000 strokes, and 60,000 new cases of Parkinson's diagnosed. Today 5.1 million Americans have Alzheimer's disease with over 650,000 under age 65. But it won't happen to you, right?

The Government Accounting Office (GAO) reports that over 60% of Americans will need long term care. Do you want to be the one that needs long term care and pays out of savings an average of $220,000, or be the one that is insured?

If you don't have LTC insurance yet you are self-insured and is that what you really want to do?

Take just 5 seconds and think about what would be the consequences to you and those around you if it happened to you?

Smaller families, high migration patterns, more women in the workplace, and increased longevity mean a family member is less likely to be available as a caregiver, while you are more likely to need long term care in the future.

Medicare, MedSup/Medigap (Medicare supplemental insurance), and traditional health (HMO, PPO) and disability insurance plans do not typically cover long term care. Persons who may be able to afford long term care through their income and personal savings represent a small minority of U.S. citizens. For most people, the options for financing long term care are long term care insurance or Medicaid, after spending down personal assets.

Most people start thinking about insuring for long term care in their 50s mainly because their parents or even some friends have required long term care. The fact is that you could need it at any age. 40% of all people receiving long term care are 18-64. Studies show that people are using their LTC insurance multiple times, for example when recovering from a car accident or surgery.

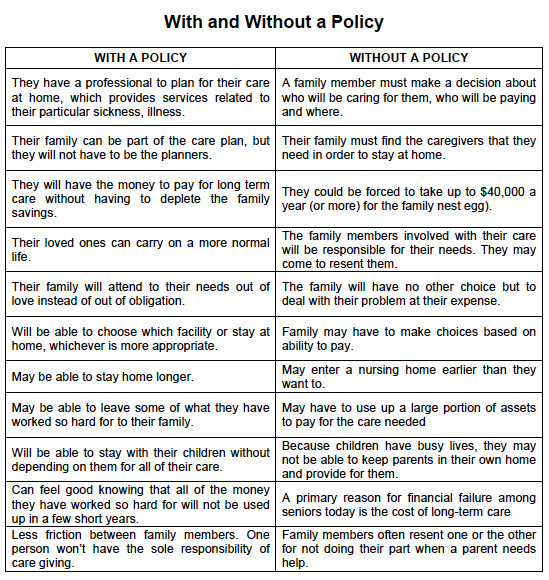

The #1 reason given for buying LTC insurance is to not be a burden on family and friends. There are many ways that LTC insurance will protect your family and friends.

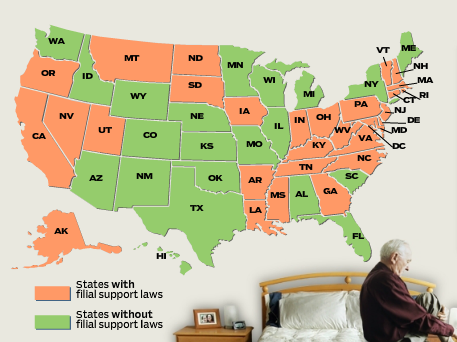

| Do You Want To Burden Your Children? Filial States: where families can be made responsible for a family member in care. Medicaid can go after family assets for repayment of care costs. |

|

Whatever age you are get a quote today... and if you can qualify, get insured, it will never be any cheaper.

The saying "if you fail to plan, you plan to fail," couldn't be more true here. Even in Superman's (Chris Reeves) case there is no warning before your health changes.

A change of health that would disqualify you from insurance doesn't have to be a disabling major illness like Parkinson's (avg. onset age 60), or stroke (28% of stroke patients are under 65), or a TIA (mini-stroke). Recent studies show that women are twice as likely to have a mid-life stroke.

A health change could be that you are diagnosed with Type II diabetes, heart problems, high blood pressure or simply being overweight and if any one of these were serious enough or were in combination with other health problems would mean you're uninsurable and on the road to self-pay and/or Medicaid (welfare).

In our experience with thousands of people, most people believe they are fine and they are not likely to need long term care, but half of them will. For some reason they think they can predict the future, but we know they can't. They are willing to risk everything they've worked for. Are you?

You will be pre-qualified when you request a quote. The only way to see if you can actually qualify is to apply. That is because the insurance company needs to review your medical records to decide if they'll insure you. A physical is not required in most cases if you've seen a doctor within the last two years.

If you are thinking about insuring for long term care you should do it about a month before your health changes because it takes about a month to get qualified. Once you have insurance if your health changes it's not a problem, you're covered.

Long term care insurance isn't for those who do not have assets at risk. Someone without assets and income is already on the road to Medicaid. Long term care insurance is to protect those with assets from ending up on Medicaid.

Doesn't it make sense to take that small amount and use it to protect the entire account? It is likely you will either pay now for insurance or pay later for care out of your savings/investments. It's your money, it's your choice.

Regulations for long term care insurance do not allow policies to be sold online but you can get a quote by email. We are able to answer any questions you may have about your quote or the insurance plans by email or phone.

All it takes is about 5 minutes of your time to see if you can pre-qualify, not everyone can. Think about the consequences to those around you if you needed long term care. Long term care insurance isn't just for you, it's for your entire family.

If you want to apply to see if you qualify, we send you the application and go over it over the phone. We have helped thousands of people protect their life savings this way. There is no risk to you. We only deal with the largest companies to make sure you have the safest future.

You should also know that you are not locked in once you apply. Every state has a 30 day period from the time you receive the policy to cancel, there is no risk to you to see if you are insurable. This insurance could save your family from the devastation of long term care.

Some people say that even at a high risk of 50:50 they may never use the insurance. What insurance do they currently have that they are looking forward to using?

People request a quote is to see how much the insurance will cost. Once they find out most people will procrastinate because no one looks forward to buying insurance.

Then a day, a month, or a year later some will have a change of health. Now they can't buy (good) insurance at any price. Do you want to be in that group or the group that is protecting their assets and in turn protecting their family?

Most Prefer Online Meetings

For over ten years we have offered online meetings. The feedback has been that it is informative and unintrusive. With an online meeting you would be at your computer and you view what is on our computer screen with screen-sharing. An advantage with an online meeting is that companies configure plans differently.

Meeting online is very simple, millions do it for business every day. This is not a video chat, we only screen share, you can see our screen but we can't see yours. At the meeting time a broker will call you and also email instructions to connect online.

We will be looking at different companies to compare plans and prices. This is not a seminar but a Q&A meeting to answer all your questions.

You will need to connect to the meeting on your computer. It is easier to show than to explain!

Schedule an online meeting today for your future protection.

Get a quote.

|

_______ |

REQUEST A QUOTE !

— The best rates as of — |